10 Common Corporate Tax Filing Mistakes and How to Avoid Them

Corporate tax filing is a responsibility of all businesses in the UAE!. However, many companies—big and small—make costly mistakes when filing corporate taxes.

These errors can lead to penalties, audits, and financial setbacks. Understanding these common pitfalls will help your business avoid them, saving it from unnecessary troubles.

In this blog post we are going to talk about the ten most common corporate tax filing mistakes. We will also tell you about the ways to avoid them.

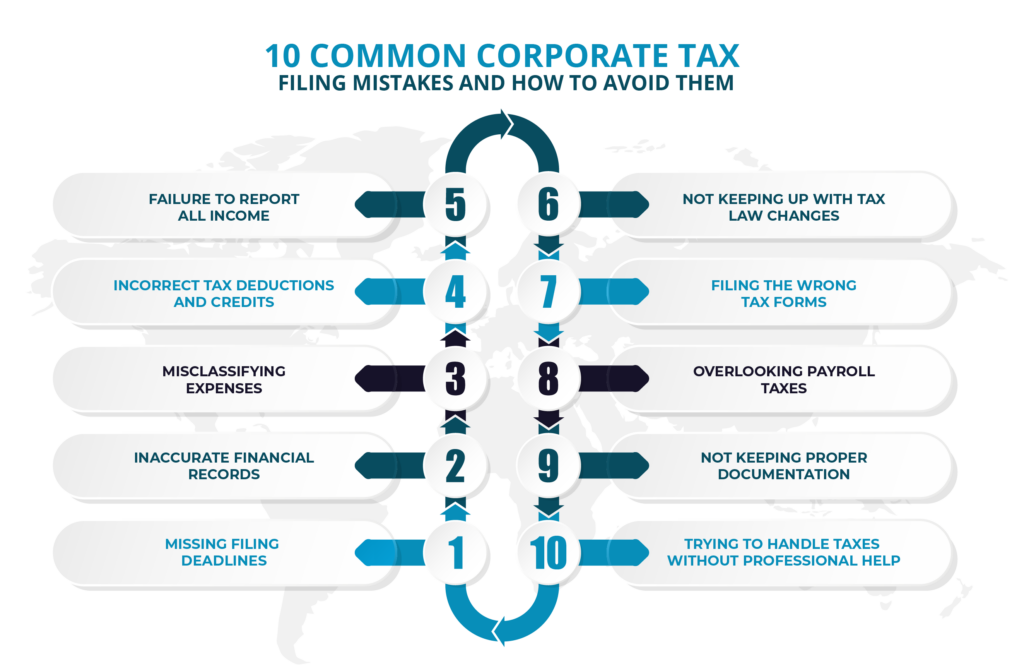

Missing Filing Deadlines

One of the most frequent mistakes businesses make is missing tax filing deadlines. Late filings can result in penalties, interest charges, and potential legal complications.

How to Avoid It

Mark tax filing deadlines on a calendar. You should also set reminders well in advance.

Work with a tax professional for timely filing.

Prepare tax documents early to avoid last-minute issues.

Inaccurate Financial Records

Poor record-keeping can lead to incorrect tax filings. Inaccurate financial data also results in underreporting or overreporting taxable income. This leads to missed deductions.

How to Avoid It

Mark tax filing deadlines on a calendar. You should also set reminders well in advance.

Work with a tax professional for timely filing.

Prepare tax documents early to avoid last-minute issues.

Inaccurate Financial Records

Poor record-keeping can lead to incorrect tax filings. Inaccurate financial data also results in underreporting or overreporting taxable income. This leads to missed deductions.

How to Avoid It

Maintain organized and updated financial records throughout the year.

Use accounting software to track expenses.

Conduct regular internal audits.

Misclassifying Expenses

Improper expense classification can lead to errors in tax calculations. Some businesses mistakenly categorize personal expenses as business expenses or fail to classify deductible expenses correctly.

How to Avoid It

Clearly separate personal and business expenses.

Consult a tax expert who can properly classify expenses.

Keep detailed records of all business-related transactions.

Incorrect Tax Deductions and Credits

Many businesses either fail to claim eligible tax deductions or claim them incorrectly. This can result in audits by tax authorities.

How to Avoid It

Stay updated on the latest tax deductions available for businesses.

Work with a tax professional for getting accurate deductions.

Keep proper documentation to substantiate all claims.

Failure to Report All Income

Underreporting income is a serious offense even if it’s accidental. No is a serious offense. Businesses that fail to report all revenue sources risk facing audits, fines, or legal actions.

How to Avoid It

Keep thorough records of all revenue streams, including cash payments and digital transactions.

Cross-check income statements against bank records and invoices.

Checking third-party payments (e.g., through PayPal, Stripe, etc.) are properly accounted for.

Not Keeping Up with Tax Law Changes

Tax regulations frequently change. Failing to stay updated can result in missed opportunities for tax benefits.

How to Avoid It

Regularly consult tax professionals or subscribe to tax news updates.

Attend business tax events.

Work with a financial advisor who specializes in corporate tax laws

Looking for corporate tax filing services?

MHR services includes Audit & Assurance, Financial Accounting, Financial & Business Advisory, Taxation including VAT, Corporate Tax & Excise Tax, Company Setup, regulatory & compliance and Management Consultancy.

Filing the Wrong Tax Forms

Different business structures require different tax forms. Filing the incorrect form can delay processing or lead to unnecessary tax liabilities.

How to Avoid It

Identify the correct tax form for your business type (e.g. corporations, for partnerships).

Consult with a tax advisor for the correct form selection.

Double-check all forms before submission to avoid errors.

Overlooking Payroll Taxes

Payroll tax errors can be costly, leading to penalties. Common mistakes include failing to withhold the correct amount or missing payroll tax filing deadlines.

How to Avoid It

Use payroll software or work with a payroll service provider.

Regularly review payroll tax requirements.

Make timely deposits of payroll taxes to avoid penalties.

Not Keeping Proper Documentation

Failing to maintain supporting tax documents can cause issues during audits. Missing records may result in denied deductions or penalties.

How to Avoid It

Keep copies of all tax returns, receipts, invoices, and supporting documents for at least seven years.

Use cloud storage-keeping systems for easy access.

Check if all records are well- categorized properly.

Trying to Handle Taxes Without Professional Help

Many business owners attempt to manage corporate tax filing themselves to save money but end up making costly errors due to a lack of expertise.

How to Avoid It

Hire a qualified tax professional.

Use trusted accounting software if managing taxes independently.

Conduct an annual tax review with a specialist to identify potential issues.

FAQs

What are the most common corporate tax filing mistakes?

Errors include miscalculations, missing deadlines, incorrect deductions, and incomplete documentation.

How can businesses avoid late tax filing penalties?

Stay updated on deadlines, set reminders, and prepare documents in advance.

What happens if a business under reports its income?

Underreporting can lead to penalties, audits, and legal consequences.

Why is accurate expense tracking important for tax filing?

Incorrect expense claims can lead to rejected deductions and possible fines.

How can businesses ensure correct tax calculations?

Use reliable accounting software or consult a tax professional.

What are common deduction mistakes businesses make?

Claiming ineligible expenses, missing allowable deductions, or misclassifying costs.

How does incorrect VAT filing affect corporate tax?

Mistakes in VAT reporting can trigger audits and financial penalties.

What documents are essential for corporate tax filing?

Financial statements, invoices, expense records, and tax returns.

How can businesses prevent tax compliance errors?

Regular audits, professional advice, and up-to-date tax knowledge.

Why should companies consult a tax expert?

Experts help minimize errors, maximize deductions, and ensure full compliance.

Conclusion

That’s a wrap for ‘10 Common Corporate Tax Filing Mistakes and How to Avoid Them’

Corporate tax filing mistakes can lead to serious legal consequences.

By staying proactive, keeping accurate records, and working with tax professionals, businesses can minimize errors.

Lastly, avoiding these common pitfalls will not only save time and money but also provide peace of mind in managing corporate tax obligations.