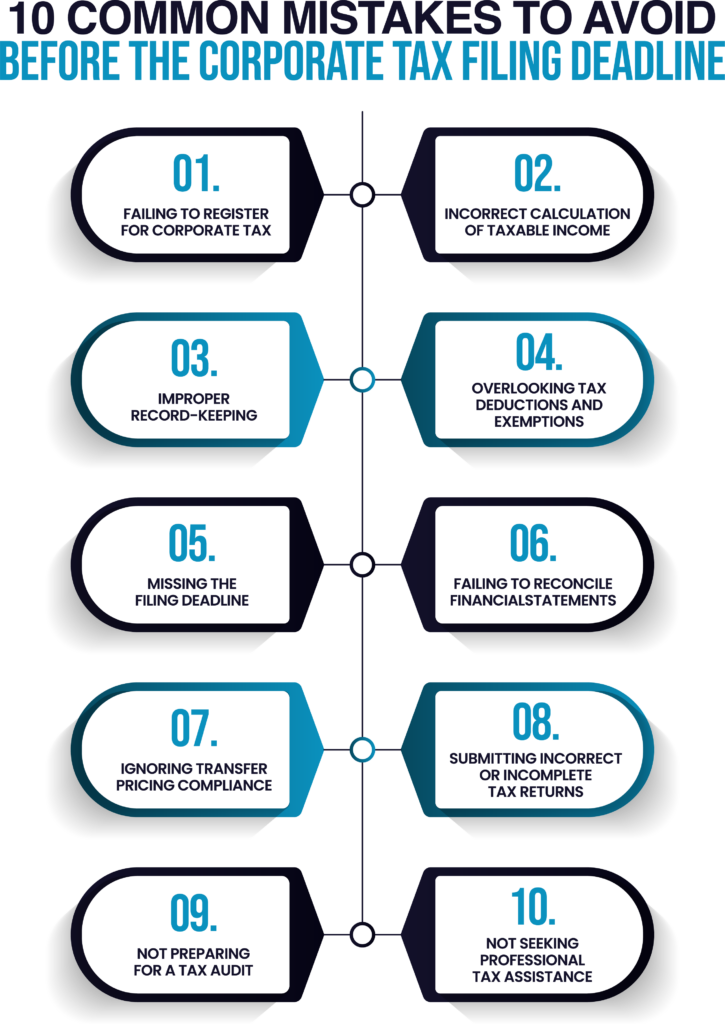

Missing the tax filing deadline can result in penalties, interest charges, and increased scrutiny from the Federal Tax Authority (FTA). It’s essential to submit your corporate tax return within nine months from the end of your financial year to remain compliant.

Registration on this portal is mandatory for Designated Non-Financial Businesses and Professions (DNFBPs) to report suspicious activities, as stipulated by Federal Decree Law No (20) of 2018 and Article 20(2) of Cabinet Decision No (10) of 2019.