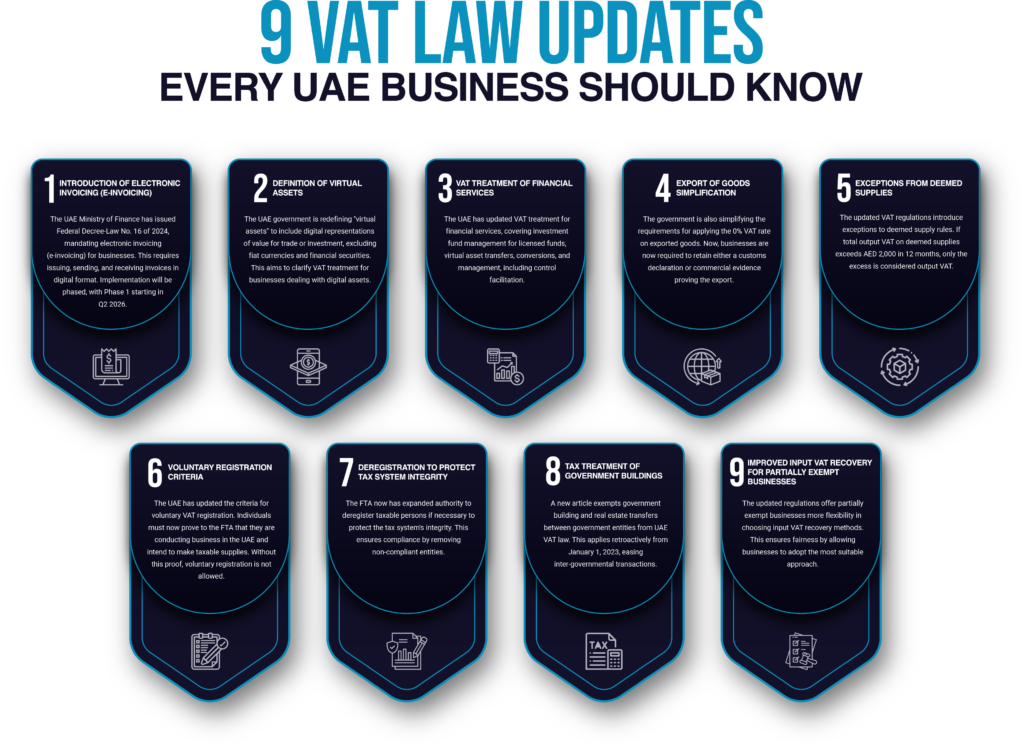

The UAE Ministry of Finance issued Federal Decree-Law No. 16 of 2024, amending key provisions of the VAT law. These amendments introduce a roadmap for implementing electronic invoicing (e-invoicing) in the UAE, with Phase 1 of e-invoicing reporting scheduled for the second quarter of 2026.

The implementation of e-invoicing aims to streamline tax reporting, reduce errors, and lower compliance costs. Businesses will need to adapt their invoicing systems to comply with the new electronic requirements, ensuring accurate and timely submission of tax invoices.

On October 2, 2024, the Federal Tax Authority (FTA) published Cabinet Decision No. 100 of 2024, amending the VAT Executive Regulations. These amendments, effective from November 15, 2024, include over 30 changes impacting various industries, aiming to enhance clarity and compliance within the VAT system.

The updated regulations introduce a new definition of virtual assets, described as “digital representation of value that can be digitally traded or converted and can be used for investment purposes, excluding digital representations of fiat currencies or financial securities.” This clarification affects the VAT treatment of transactions involving virtual assets.

The amendments to Article 30 of the VAT law provide clearer guidelines on the VAT treatment of exports, including the application of zero-rating and the documentation required to substantiate export transactions. Businesses engaged in export activities should review these changes to ensure compliance.

The updated regulations offer more detailed provisions regarding the VAT treatment of financial services, including exemptions and the allocation of input tax credits. Financial institutions and related service providers should assess these changes to understand their impact on operations.

Businesses should conduct a thorough review of the updated VAT laws and regulations, assess the impact on their operations, and update internal processes and systems accordingly. Engaging with tax professionals can provide valuable guidance to navigate these changes effectively.